If you’ve spent any time in the past few years in the real estate marketplace, then you are well familiar with the current real estate problem. Starting in 2006, the sub prime crisis came to ahead when the real estate market and lending industry realized that years of careless lending were starting to hurt. This led to the foreclosure epidemic, which in turn had a hand to play in the great recession of 2008.

This is likely information you are already aware of, but what you may not know is the government’s proposed solution to this crisis. After spending a significant amount of time, and money, trying to place blame in the situation, the government then decided to come up with a solution, which presented itself in the Dodd-Frank Wall Street Reform and Consumer Protection Act.

While it may not look as though this act has anything to do with real estate, if you are pursuing a loan in 2014, it will. Dodd-Frank created the Consumer Financial Protection Bureau, which is an independent federal agency that is given broad power to oversee financial products and services, and this includes mortgages.

After 18 months trying to determine what caused the sub-prime crisis, the CFPB has created around 900 new regulatory provisions which are designed to protect you from not only the mortgage industry, but also yourself. Because the changes go into effect on New Year’s Day in 2014, it’s important for those considering entering the home buying process to understand these.

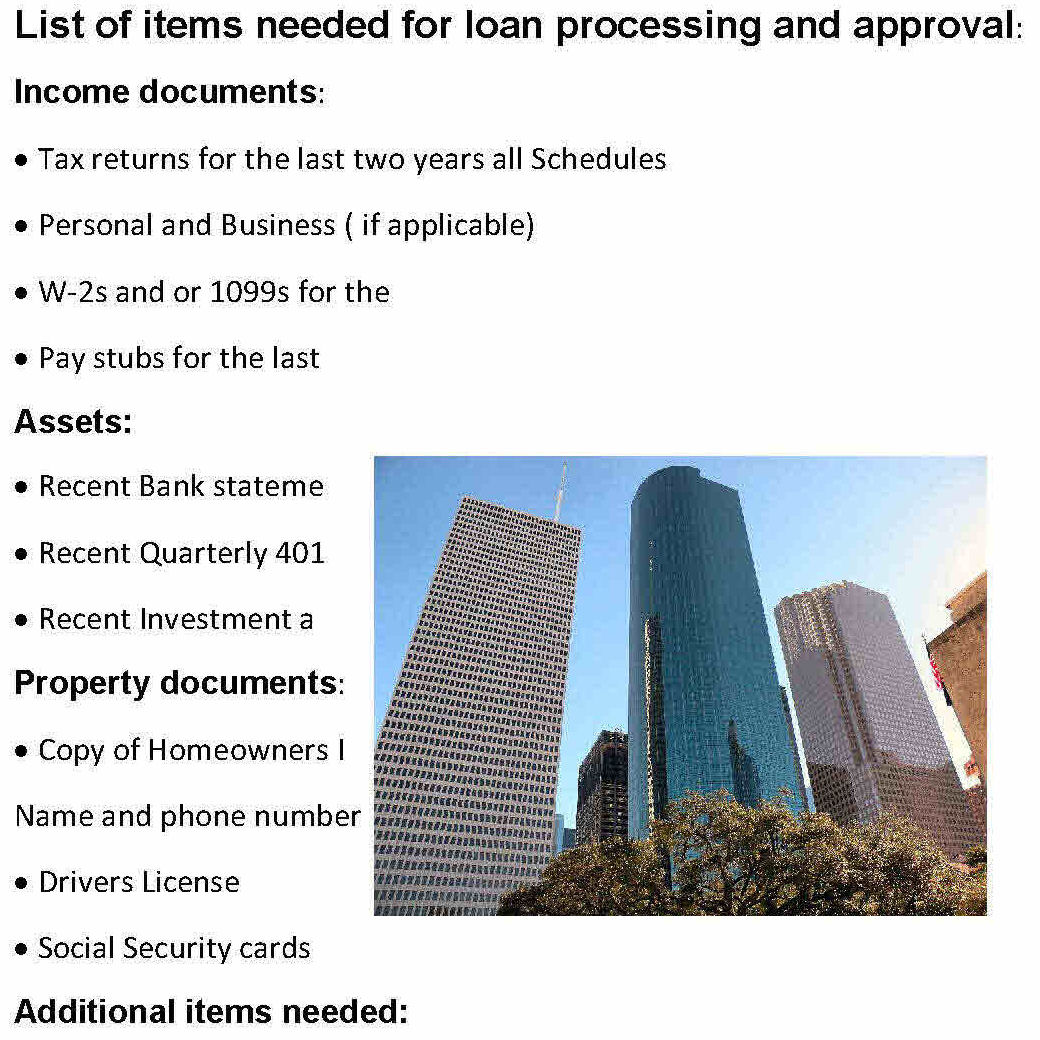

The changes that affect borrowers in the Houston real estate market directly are the changes to the qualification requirements. One of the main changes is the impart your debt-to-income ratio will have on your ability to get a mortgage. The CFBP regulations enforce stronger “ability-to-pay” rules, and now borrowers cannot get a mortgage if their debt-to-income ratio exceeds 43 percent. In addition, you will have to prove your financial standing with bank statements, proof of assets, employment status reports, pay stubs and your credit history.

In addition to making it more challenging for iffy borrowers to qualify for a mortgage, the new regulations limit risky loans, such as those that extend beyond 30 years, or loans that offer an interest only teaser rate. Finally, lenders are going to have to be more open and honest with borrowers about what their mortgage payments are going towards.

So what does this mean for you? If you are a borrower in good credit with a solid handle on your debts and a good income, you should have no trouble getting a loan. If you are a risky borrower, you are going to want to start working now towards solidifying your financial situation, unfortunately, with the new regulations, it is going to be harder for you to get a loan in 2014.

Changes are coming in 2014, and you need to understand them. If you have any further questions about how these regulations will affect your home buying in the Houston real estate market, contact Bill Edge for help from an experienced real estate Broker who has taken the time to learn about these regulations and qualification requirements.

Have a question about a property? Want to learn more about the Houston Real Estate Market? Ready to tour your favorite homes today? Contact Inner Loop Realtor Bill Edge now.

Title: CFPB loan requirements affect Houston home buyers in 2014